Guys this idea is really like looking at tea leaves, you can see anything in a historical chart as the human tries to make sense of the randomness of it. But really the ML should be able to take into consideration far more numbers of features that a human can (such as price action) and hence overall in theory you would expect it to win. But you have to be trading over short time frames (relative to your market) so that external factors or manipulation of markets have less impact. My ML has around 800 features to build models from but I am refactoring the features into a reduced set to reduce overfitting of the models. Also you need to support very good trading adaptability to dynamically adapt trading strategies to suit market conditions and it goes without saying that whatever algorithm you use you must have excellent equity management, appropriate types of orders, hedging strategies etc. All my bots, ML/grid have this as standard.

Is it possible to teach the bot, for example, through a very large number of profitable transactions presented visually, where there are several indicators on the charts, or on this basis you can program the bot to draw conclusions / assumptions of entry and exit by itself ?

So sorry mate its very very simple, my limit order target pips for my bot is 1 pip and when I run the bot live I usually get around 1 pip successful trade results. However I also get more losing trades in terms of amounts than winners so the bots lose. But on backtest I never get the 1 pip target but usually get 4 pips of more and get a lot more winners than losers!

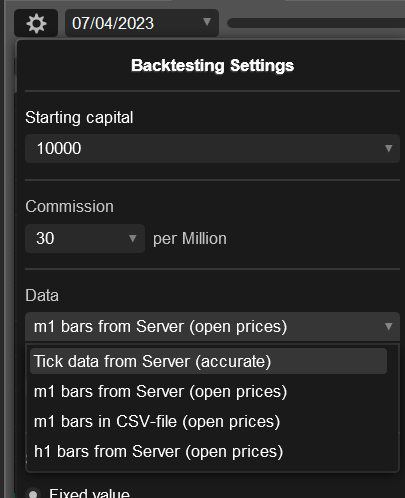

The target pips for my limit orders is only 1 pip and on live the winning orders are around the 1 pip amount. But on the backtesting the limit orders take much more than that. This might be caused by there being a lot less data on backtesting than on live?

RE: RE: RE: Targets different on backtest and live

So sorry mate its very very simple, my limit order target pips for my bot is 1 pip and when I run the bot live I usually get around 1 pip successful trade results. However I also get more losing trades in terms of amounts than winners so the bots lose. But on backtest I never get the 1 pip target but usually get 4 pips of more and get a lot more winners than losers!

The target pips for my limit orders is only 1 pip and on live the winning orders are around the 1 pip amount. But on the backtesting the limit orders take much more than that. This might be caused by there being a lot less data on backtesting than on live?

The target pips for my limit orders is only 1 pip and on live the winning orders are around the 1 pip amount. But on the backtesting the limit orders take much more than that. This might be caused by there being a lot less data on backtesting than on live?

acrigney

19 Jan 2024, 06:53

( Updated at: 21 Jan 2024, 11:24 )

RE: RE: RE: RE: CBot instance XXX process was unexpectedly terminated.

OK mate I did a submit with the issue but I think I found that if I do a build inside CTrader it will then work. So something was out of sync perhaps with VS and2022 and Ctrader perhaps?

Thanks mate but I don't see how that is going to help you, maybe if I could send you a stack trace/symbolic dump or something?

The error occurs before the bot gets to debug. I have tried a clean rebuild etc. I just cloned one bot to make changes and it happened after making changes to the clone. I will reclone again and see if I get the problem again before making any changes.

Thanks mate but I don't see how that is going to help you, maybe if I could send you a stack trace/symbolic dump or something?

The error occurs before the bot gets to debug. I have tried a clean rebuild etc. I just cloned one bot to make changes and it happened after making changes to the clone. I will reclone again and see if I get the problem again before making any changes.

acrigney

17 Jan 2024, 12:08

( Updated at: 18 Jan 2024, 14:11 )

RE: CBot instance XXX process was unexpectedly terminated.

Thanks mate but I don't see how that is going to help you, maybe if I could send you a stack trace/symbolic dump or something?

The error occurs before the bot gets to debug. I have tried a clean rebuild etc. I just cloned one bot to make changes and it happened after making changes to the clone. I will reclone again and see if I get the problem again before making any changes.

Yes I am doing that, on live demo the trades didn't match the backtest trades. And on range bars you backtest with the range bars you are using, its in the drop down, I didn't know that before either.

Thanks mate the problem was that on Range bars I could not use expiry times for my orders. Also on backtesting I could not run all of my ML models in parrallel that use time bars, I have an ensemble of models for them. But I guess they would work on live though but I can't really have bots that you can backtest and bots that you can't. But the Range bar model looks really good on the backtest and I can still ensemble it with other models., I am using a model generaled on the 5 tick range with almost 2 years of data.

If you help us reproduce this, we might be able to spot the issue for you

Thanks mate are you saying that I should be able to use orders with expiry times on Range charts? And with backtesting on a 5 pip range, will I get all of the data as my bots missed most of the trades on live that I got during backtesting.

Thanks mate the problem was that on Range bars I could not use expiry times for my orders. Also on backtesting I could not run all of my ML models in parrallel that use time bars, I have an ensemble of models for them. But I guess they would work on live though but I can't really have bots that you can backtest and bots that you can't. But the Range bar model looks really good on the backtest and I can still ensemble it with other models., I am using a model generaled on the 5 tick range with almost 2 years of data.

acrigney

04 Oct 2023, 03:12

( Updated at: 04 Oct 2023, 05:38 )

RE: 18000% backtesting bot doesn't perform good on live trading

Mate but if we want our code to run on minutes (i.e. not on ticks) then is it legitimate to backtest on minutes. Or should we backtest on ticks but convert the ticks to minute bars? When I capture the data on ticks live its a lot more than what you get on backtesting and I think on minute trading but I need to check.

I don't think this latest version is very stable, my bots often show that they need to be rebuilt and my code builds but the .algo code is not created. Was there another big upgrade?

I am using .net 6 bots with the VS2022 17.5.4 not any preview versions. but I will upgrade now.

Guys I was copying some providers on demo accounts and the same thing happened. They were doing really well then they lost the account. I asked Ctrader if they would add a loss catching feature. I have that in all of my bots. I build ML and grid based bots.

b.lazarecki said:

Unfortunately I was testing it with real money and lost over 70% of deposit. When I join copy I didn't see that there are a lot of losing positions already opened. So without opening new ones somehow I ve joined losing ones. Withing 5 hours I've lost more than 70%.

Awesome thanks heaps mate, you have really saved my bacon!! What kind of bots do you build? I build ML ones.

firemyst said:

> So sorry gus yes it worked with FullAccess using the launch debugger but it does not work with trying to attach, that is the normal way I try and do it with my bots.

> It says symbols have not been loaded. Looks like you have to specify the location of the symbols but I have never had to do that before.

Because everything now runs under its own process, you could have literally hundreds of calgo processes running, and wouldn't know which one to attach to.

The new way of debugging automatically handles that for you. When prompted, select the VS instance you're currently working in (as per the instructions on the web page) making sure you're running it in "debug" mode, and you'll be able to step through the code as per usual.

acrigney

23 Dec 2024, 10:08

RE: "ChatGpT like" machine learning AI

Guys this idea is really like looking at tea leaves, you can see anything in a historical chart as the human tries to make sense of the randomness of it. But really the ML should be able to take into consideration far more numbers of features that a human can (such as price action) and hence overall in theory you would expect it to win. But you have to be trading over short time frames (relative to your market) so that external factors or manipulation of markets have less impact. My ML has around 800 features to build models from but I am refactoring the features into a reduced set to reduce overfitting of the models. Also you need to support very good trading adaptability to dynamically adapt trading strategies to suit market conditions and it goes without saying that whatever algorithm you use you must have excellent equity management, appropriate types of orders, hedging strategies etc. All my bots, ML/grid have this as standard.

gnsmaciej said:

@acrigney