Indicator not moving along with time passes

Joined 03.06.2020

Indicator not moving along with time passes

20 Apr 2022, 04:42

Hello,

If anyone could help me to sort out a strange problem. Details as below, thanks.

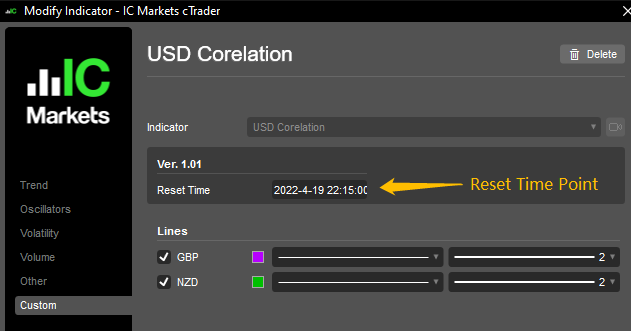

I want to make 2 indicators, which will show GBPUSD and NZDUSD movement in the chart of EURUSD in a low timeframe (e.g 3min). Both indicators will be aligned with EURUSD at a time point, which I call 'Reset Time Point' as below screen chop:

The problem is that the GBP indicator works very well, but NZD doesn't. See the below explanation:

The sample code is attached below:

using System;

using cAlgo.API;

using cAlgo.API.Internals;

namespace cAlgo

{

[Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class USDCorelation : Indicator

{

[Parameter("Reset Time", DefaultValue = "2022-4-19 22:15:00", Group = "Ver. 1.01")]

public string ResetPoint { get; set; }

[Output("GBP", LineColor = "FFB600FF", Thickness = 2, PlotType = PlotType.DiscontinuousLine)]

public IndicatorDataSeries GBP { get; set; }

[Output("NZD", LineColor = "FF00BF00", Thickness = 2, PlotType = PlotType.DiscontinuousLine)]

public IndicatorDataSeries NZD { get; set; }

private DateTime dt_RstPnt; //Reset Time Point;

//Bars to load for Calculate

private Bars EURUSD, GBPUSD, NZDUSD;

//Index at ResetTimePoint of EachSymbol;

private int in_EURUSD, in_GBPUSD, in_NZDUSD;

//BaseValue at ResetTimePoint of EachSymbol;

private double db_EURUSD, db_GBPUSD, db_NZDUSD;

//BarNumber from ResetTimePoint to LastBar

private int gap;

protected override void Initialize()

{

//1.Get MarketData in Series Ready

EURUSD = MarketData.GetBars(Bars.TimeFrame, "EURUSD");

GBPUSD = MarketData.GetBars(Bars.TimeFrame, "GBPUSD");

NZDUSD = MarketData.GetBars(Bars.TimeFrame, "NZDUSD");

//2.Get ResetTimePoint Index

dt_RstPnt = DateTime.Parse(ResetPoint).Add(-Application.UserTimeOffset);

in_EURUSD = EURUSD.OpenTimes.GetIndexByTime(dt_RstPnt);

in_GBPUSD = GBPUSD.OpenTimes.GetIndexByTime(dt_RstPnt);

in_NZDUSD = NZDUSD.OpenTimes.GetIndexByTime(dt_RstPnt);

//3.Get OpenPrice of each symbol at ResetTimePoint

db_EURUSD = EURUSD[in_EURUSD].Open;

db_GBPUSD = GBPUSD[in_GBPUSD].Open;

db_NZDUSD = NZDUSD[in_NZDUSD].Open;

}

public override void Calculate(int index)

{

gap = index - in_EURUSD;

GBP[index] = ((GBPUSD[in_GBPUSD + gap].Close) + db_EURUSD - db_GBPUSD);

NZD[index] = ((NZDUSD[in_NZDUSD + gap].Close) + db_EURUSD - db_NZDUSD);

}

}

}

Replies

Capt.Z-Fort.Builder

20 Apr 2022, 13:34

RE:

Thank you like always, it works perfectly. :)

amusleh said:

Hi,

Try this:

using System; using cAlgo.API; using cAlgo.API.Internals; namespace cAlgo { [Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)] public class USDCorelation : Indicator { [Parameter("Reset Time", DefaultValue = "2022-4-19 22:15:00", Group = "Ver. 1.01")] public string ResetPoint { get; set; } [Output("GBP", LineColor = "FFB600FF", Thickness = 2, PlotType = PlotType.DiscontinuousLine)] public IndicatorDataSeries GBP { get; set; } [Output("NZD", LineColor = "FF00BF00", Thickness = 2, PlotType = PlotType.DiscontinuousLine)] public IndicatorDataSeries NZD { get; set; } private DateTime dt_RstPnt; //Reset Time Point; //Bars to load for Calculate private Bars EURUSD, GBPUSD, NZDUSD; //Index at ResetTimePoint of EachSymbol; private int in_EURUSD, in_GBPUSD, in_NZDUSD; //BaseValue at ResetTimePoint of EachSymbol; private double db_EURUSD, db_GBPUSD, db_NZDUSD; protected override void Initialize() { //1.Get MarketData in Series Ready EURUSD = MarketData.GetBars(Bars.TimeFrame, "EURUSD"); GBPUSD = MarketData.GetBars(Bars.TimeFrame, "GBPUSD"); NZDUSD = MarketData.GetBars(Bars.TimeFrame, "NZDUSD"); //2.Get ResetTimePoint Index dt_RstPnt = DateTime.Parse(ResetPoint).Add(-Application.UserTimeOffset); in_EURUSD = EURUSD.OpenTimes.GetIndexByTime(dt_RstPnt); in_GBPUSD = GBPUSD.OpenTimes.GetIndexByTime(dt_RstPnt); in_NZDUSD = NZDUSD.OpenTimes.GetIndexByTime(dt_RstPnt); //3.Get OpenPrice of each symbol at ResetTimePoint db_EURUSD = EURUSD[in_EURUSD].Open; db_GBPUSD = GBPUSD[in_GBPUSD].Open; db_NZDUSD = NZDUSD[in_NZDUSD].Open; } public override void Calculate(int index) { if (Bars.OpenTimes[index] < dt_RstPnt) return; var gbpIndex = GBPUSD.OpenTimes.GetIndexByTime(Bars.OpenTimes[index]); var gbpGap = gbpIndex - in_GBPUSD; GBP[index] = ((GBPUSD[in_GBPUSD + gbpGap].Close) + db_EURUSD - db_GBPUSD); var nzdIndex = NZDUSD.OpenTimes.GetIndexByTime(Bars.OpenTimes[index]); var nzdGap = nzdIndex - in_NZDUSD; NZD[index] = ((NZDUSD[in_NZDUSD + nzdGap].Close) + db_EURUSD - db_NZDUSD); } } }

@Capt.Z-Fort.Builder

amusleh

20 Apr 2022, 09:23

Hi,

Try this:

@amusleh