Custom indicators not appearing under reference manager

Joined 27.12.2024

Custom indicators not appearing under reference manager

27 Dec 2024, 16:22

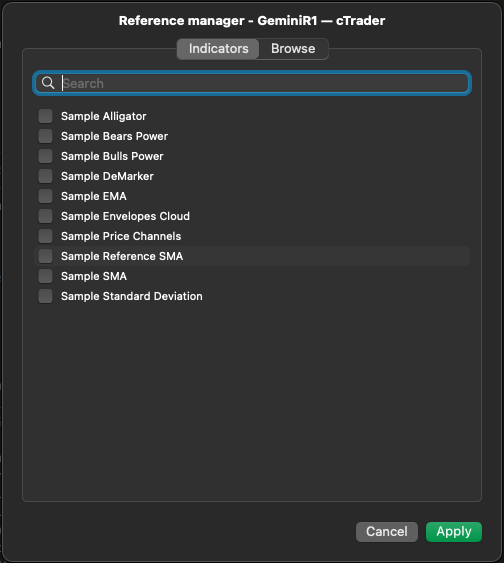

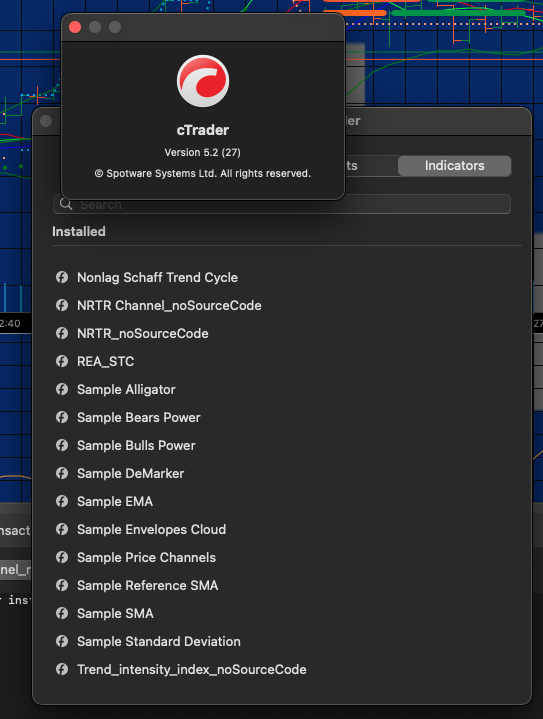

Kindly assist my custom indicators are not appearing under reference manager in “Algo”. So I can't use them in my cBots.

However they do appear under “trade” when I want to add them to charts

The custom indicators I'm referring to do not appear in the first screenshot but they do appear in the second one. I'm running Ctrader version 5.2(27).

Please help.

Replies

masedir

30 Dec 2024, 11:35

( Updated at: 02 Jan 2025, 07:06 )

RE: Custom indicators not appearing under reference manager

PanagiotisCharalampous said:

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

No, I don't have source codes. I downloaded one of them (Nonlag Schaff Trend Cycle) from clickalgo.com; The other ones I downloaded from different sites on the web.

@masedir

masedir

30 Dec 2024, 15:08

( Updated at: 02 Jan 2025, 07:06 )

RE: Custom indicators not appearing under reference manager

PanagiotisCharalampous said:

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

NRTR Channel source code

Please receive attachedusing System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo

{

[Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class NRTRChannel : Indicator

{

[Parameter("ATR Period", DefaultValue = 40)]

public int ATRPeriod { get; set; }

[Parameter("ATR Multiplier", DefaultValue = 2.0)]

public double ATRMultiplier { get; set; }

[Parameter("Show Price Labels", DefaultValue = true)]

public bool ShowLabels { get; set; }

[Output("longResistance", LineColor = "DeepSkyBlue", PlotType = PlotType.DiscontinuousLine, LineStyle = LineStyle.Dots, Thickness = 2)]

public IndicatorDataSeries CeilingBuffer { get; set; }

[Output("longSupport", LineColor = "DeepSkyBlue", PlotType = PlotType.DiscontinuousLine, LineStyle = LineStyle.Dots, Thickness = 2)]

public IndicatorDataSeries BuyBuffer { get; set; }

[Output("shortSupport", LineColor = "LightSalmon", PlotType = PlotType.DiscontinuousLine, LineStyle = LineStyle.Dots, Thickness = 2)]

public IndicatorDataSeries SellBuffer { get; set; }

[Output("shortResistance", LineColor = "LightSalmon", PlotType = PlotType.DiscontinuousLine, LineStyle = LineStyle.Dots, Thickness = 2)]

public IndicatorDataSeries FloorBuffer { get; set; }

private IndicatorDataSeries trendBuffer;

private AverageTrueRange atr;

private const int UP_TREND = 1;

private const int DOWN_TREND = -1;

protected override void Initialize()

{

trendBuffer = CreateDataSeries();

atr = Indicators.AverageTrueRange(ATRPeriod, MovingAverageType.Simple);

}

public override void Calculate(int index)

{

if (index <= ATRPeriod)

return;

if (index == ATRPeriod + 1)

{

if (Bars.ClosePrices[index] > Bars.LowPrices[index])

{

trendBuffer[index] = UP_TREND;

CeilingBuffer[index] = Bars.ClosePrices[index];

BuyBuffer[index] = Bars.ClosePrices[index] - ATRMultiplier * atr.Result[index];

}

else

{

trendBuffer[index] = DOWN_TREND;

FloorBuffer[index] = Bars.ClosePrices[index];

SellBuffer[index] = Bars.ClosePrices[index] + ATRMultiplier * atr.Result[index];

}

return;

}

if (trendBuffer[index - 1] > 0)

{

if (Bars.LowPrices[index] > CeilingBuffer[index - 1])

{

CeilingBuffer[index] = Bars.ClosePrices[index];

FloorBuffer[index] = double.NaN;

BuyBuffer[index] = Bars.ClosePrices[index] - ATRMultiplier * atr.Result[index];

SellBuffer[index] = double.NaN;

trendBuffer[index] = UP_TREND;

}

else if (Bars.ClosePrices[index] < BuyBuffer[index - 1])

{

trendBuffer[index] = DOWN_TREND;

FloorBuffer[index] = Bars.ClosePrices[index];

SellBuffer[index] = Bars.ClosePrices[index] + ATRMultiplier * atr.Result[index];

CeilingBuffer[index] = double.NaN;

BuyBuffer[index] = double.NaN;

}

else

{

CopyPreviousValues(index);

}

}

else

{

if (Bars.HighPrices[index] < FloorBuffer[index - 1])

{

FloorBuffer[index] = Bars.ClosePrices[index];

CeilingBuffer[index] = double.NaN;

SellBuffer[index] = Bars.ClosePrices[index] + ATRMultiplier * atr.Result[index];

BuyBuffer[index] = double.NaN;

trendBuffer[index] = DOWN_TREND;

}

else if (Bars.ClosePrices[index] > SellBuffer[index - 1])

{

trendBuffer[index] = UP_TREND;

CeilingBuffer[index] = Bars.ClosePrices[index];

BuyBuffer[index] = Bars.ClosePrices[index] - ATRMultiplier * atr.Result[index];

FloorBuffer[index] = double.NaN;

SellBuffer[index] = double.NaN;

}

else

{

CopyPreviousValues(index);

}

}

if (ShowLabels && index == Bars.ClosePrices.Count - 1)

{

ShowPriceLevels(index);

}

}

private void CopyPreviousValues(int index)

{

SellBuffer[index] = SellBuffer[index - 1];

BuyBuffer[index] = BuyBuffer[index - 1];

CeilingBuffer[index] = CeilingBuffer[index - 1];

FloorBuffer[index] = FloorBuffer[index - 1];

trendBuffer[index] = trendBuffer[index - 1];

}

private void ShowPriceLevels(int index)

{

var existingLabels = Chart.Objects.Where(obj => obj.Name.StartsWith("NRTR_"));

foreach (var label in existingLabels)

{

Chart.RemoveObject(label.Name);

}

cAlgo.API.Color color;

double upperLevel, lowerLevel;

if (trendBuffer[index] == UP_TREND)

{

color = cAlgo.API.Color.DeepSkyBlue;

upperLevel = CeilingBuffer[index];

lowerLevel = BuyBuffer[index];

}

else

{

color = cAlgo.API.Color.LightSalmon;

upperLevel = SellBuffer[index];

lowerLevel = FloorBuffer[index];

}

if (!double.IsNaN(upperLevel))

{

var upperText = Chart.DrawText(

"NRTR_Res_" + index,

upperLevel.ToString("F5"),

index,

upperLevel,

color

);

upperText.VerticalAlignment = VerticalAlignment.Center;

upperText.HorizontalAlignment = HorizontalAlignment.Right;

}

if (!double.IsNaN(lowerLevel))

{

var lowerText = Chart.DrawText(

"NRTR_Sup_" + index,

lowerLevel.ToString("F5"),

index,

lowerLevel,

color

);

lowerText.VerticalAlignment = VerticalAlignment.Center;

lowerText.HorizontalAlignment = HorizontalAlignment.Right;

}

}

}

}@masedir

masedir

30 Dec 2024, 15:10

( Updated at: 02 Jan 2025, 07:06 )

RE: Custom indicators not appearing under reference manager

PanagiotisCharalampous said:

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

Trend_Intensity-Index Source Code

using System;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo

{

[Indicator(IsOverlay = false, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class Trend_intensity_index : Indicator

{

[Parameter("Period", DefaultValue = 30)]

public int Period { get; set; }

[Parameter("MA Method", DefaultValue = MovingAverageType.Simple)]

public MovingAverageType MAMethod { get; set; }

[Parameter("Upper Level", DefaultValue = 80.0)]

public double LevelHigh { get; set; }

[Parameter("Lower Level", DefaultValue = 20.0)]

public double LevelLow { get; set; }

[Output("tii", LineColor = "Gray", PlotType = PlotType.Line, Thickness = 2)]

public IndicatorDataSeries TII { get; set; }

[Output("upperBand", LineColor = "DeepSkyBlue", PlotType = PlotType.Line)]

public IndicatorDataSeries UpperBand { get; set; }

[Output("lowerBand", LineColor = "SandyBrown", PlotType = PlotType.Line)]

public IndicatorDataSeries LowerBand { get; set; }

[Output("level", LineColor = "DarkGray", PlotType = PlotType.Line)]

public IndicatorDataSeries Level { get; set; }

private MovingAverage maa;

private MovingAverage map;

private int maPeriod;

protected override void Initialize()

{

maPeriod = Period * 2;

maa = Indicators.MovingAverage(Bars.ClosePrices, maPeriod, MAMethod);

map = Indicators.MovingAverage(Bars.ClosePrices, 1, MAMethod);

}

public override void Calculate(int index)

{

if (index < Period)

return;

double sumUpDeviations = 0;

double sumDnDeviations = 0;

for (int k = 0; k < Period && index >= k; k++)

{

double diff = map.Result[index - k] - maa.Result[index];

if (diff > 0)

sumUpDeviations += diff;

else

sumDnDeviations -= diff;

}

double value;

if ((sumUpDeviations + sumDnDeviations) != 0)

value = 100 * sumUpDeviations / (sumUpDeviations + sumDnDeviations);

else

value = 0;

TII[index] = value;

Level[index] = (value > LevelHigh) ? 100 : (value < LevelLow) ? 0 : 50;

// Set upper and lower bands for filling

if (value > 50)

{

UpperBand[index] = value;

LowerBand[index] = Math.Min(value, LevelHigh);

}

else

{

UpperBand[index] = value;

LowerBand[index] = Math.Max(value, LevelLow);

}

}

}

}@masedir

masedir

02 Jan 2025, 16:46

RE: RE: Custom indicators not appearing under reference manager

masedir said:

PanagiotisCharalampous said:

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

No, I don't have source codes. I downloaded one of them (Nonlag Schaff Trend Cycle) from clickalgo.com; The other ones I downloaded from different sites on the web.

The two indicators that I have provided source code for can be referenced after compiling them, however the NRTRChannel gives an error below when referencing it:

Error MSB4006: There is a circular dependency in the target dependency graph involving target "_GenerateRestoreProjectPathWalk". (/usr/local/share/dotnet/sdk/8.0.303/NuGet.targets, line: 1196, column: 5)

As for the other indicators that I don't have source code for, I'm still having no luck.

@masedir

PanagiotisCharalampous

03 Jan 2025, 08:14

RE: RE: RE: Custom indicators not appearing under reference manager

masedir said:

masedir said:

PanagiotisCharalampous said:

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

No, I don't have source codes. I downloaded one of them (Nonlag Schaff Trend Cycle) from clickalgo.com; The other ones I downloaded from different sites on the web.

The two indicators that I have provided source code for can be referenced after compiling them, however the NRTRChannel gives an error below when referencing it:

Error MSB4006: There is a circular dependency in the target dependency graph involving target "_GenerateRestoreProjectPathWalk". (/usr/local/share/dotnet/sdk/8.0.303/NuGet.targets, line: 1196, column: 5)

As for the other indicators that I don't have source code for, I'm still having no luck.

Thank you, only indicators with source code can be referenced to other projects.

@PanagiotisCharalampous

PanagiotisCharalampous

30 Dec 2024, 07:25

Hi there,

Do your custom indicators have source code?

Best regards,

Panagiotis

@PanagiotisCharalampous