Description

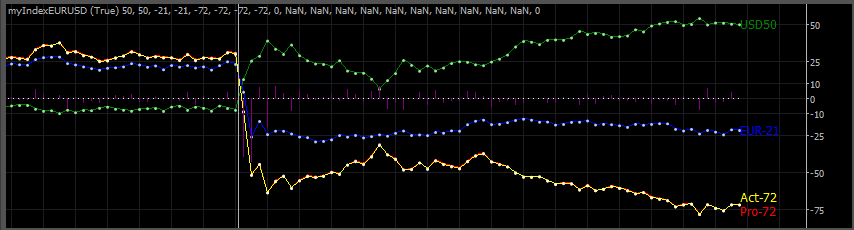

Determines the daily increase or decrease in the value of the Euro and Dollar.The actual and projected value of the pair is also plotted.

using System;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo.Indicators

{

[Indicator(IsOverlay = false, AutoRescale = true, ScalePrecision = 0, TimeZone = TimeZones.UTC)]

[Levels(-75, 75, -50, 50, -25, 25, 10, -10, 0, 100,

-100)]

public class myIndexEURUSD : Indicator

{

[Parameter(DefaultValue = false)]

public bool HideYeilds { get; set; }

[Output("USD Index", Color = Colors.Green)]

public IndicatorDataSeries USDIDX { get; set; }

[Output("USD Points", Color = Colors.LightGreen, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries USDIDXPoints { get; set; }

[Output("EUR Index", Color = Colors.Blue)]

public IndicatorDataSeries EURIDX { get; set; }

[Output("EUR Points", Color = Colors.LightBlue, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries EURIDXPoints { get; set; }

[Output("ProjYld", Color = Colors.Red)]

public IndicatorDataSeries ProjYld { get; set; }

[Output("ProjYld Points", Color = Colors.Pink, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries ProjYldPoints { get; set; }

[Output("ActYld", Color = Colors.Yellow)]

public IndicatorDataSeries ActYld { get; set; }

[Output("ActYld Points", Color = Colors.LightYellow, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries ActYldPoints { get; set; }

[Output("Delta", PlotType = PlotType.Histogram, Color = Colors.Purple)]

public IndicatorDataSeries Delta { get; set; }

//[Output("EURUSD", Color = Colors.Blue)]

//public IndicatorDataSeries Yeild1 { get; set; }

[Output("USDJPY", Color = Colors.Red)]

public IndicatorDataSeries YldUSDJPY { get; set; }

[Output("GBPUSD", Color = Colors.Yellow)]

public IndicatorDataSeries YldGBPUSD { get; set; }

[Output("AUDUSD", Color = Colors.Purple)]

public IndicatorDataSeries YldAUDUSD { get; set; }

[Output("USDCHF", Color = Colors.OrangeRed)]

public IndicatorDataSeries YldUSDCHF { get; set; }

[Output("EURJPY", Color = Colors.Pink)]

public IndicatorDataSeries YldEURJPY { get; set; }

[Output("EURGBP", Color = Colors.LightYellow)]

public IndicatorDataSeries YldEURGBP { get; set; }

[Output("EURAUD", Color = Colors.Orchid)]

public IndicatorDataSeries YldEURAUD { get; set; }

[Output("EURCHF", Color = Colors.Orange)]

public IndicatorDataSeries YldEURCHF { get; set; }

[Output("BuySignal", Color = Colors.Blue, Thickness = 5, PlotType = PlotType.Points)]

public IndicatorDataSeries BuySignal { get; set; }

[Output("SellSignal", Color = Colors.Red, Thickness = 5, PlotType = PlotType.Points)]

public IndicatorDataSeries SellSignal { get; set; }

[Output("Center", LineStyle = LineStyle.DotsRare, Color = Colors.White)]

public IndicatorDataSeries CenterLine { get; set; }

private MarketSeries msUSDJPY, msGBPUSD, msAUDUSD, msUSDCHF, msEURJPY, msEURGBP, msEURAUD, msEURCHF;

protected override void Initialize()

{

string IndicatorName = GetType().ToString().Substring(GetType().ToString().LastIndexOf('.') + 1);

// returns ClassName

Print("Indicator: " + IndicatorName);

Print("IndicatorTimeZone: {0} Offset: {1} DST: {2}", TimeZone, TimeZone.BaseUtcOffset, TimeZone.SupportsDaylightSavingTime);

msUSDJPY = MarketData.GetSeries("USDJPY", TimeFrame);

msGBPUSD = MarketData.GetSeries("GBPUSD", TimeFrame);

msAUDUSD = MarketData.GetSeries("AUDUSD", TimeFrame);

msUSDCHF = MarketData.GetSeries("USDCHF", TimeFrame);

msEURJPY = MarketData.GetSeries("EURJPY", TimeFrame);

msEURGBP = MarketData.GetSeries("EURGBP", TimeFrame);

msEURAUD = MarketData.GetSeries("EURAUD", TimeFrame);

msEURCHF = MarketData.GetSeries("EURCHF", TimeFrame);

}

public override void Calculate(int index)

{

if (index < 1)

return;

int idxEURUSD = index;

var idxUSDJPY = msUSDJPY.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxGBPUSD = msGBPUSD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxAUDUSD = msAUDUSD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxUSDCHF = msUSDCHF.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURJPY = msEURJPY.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURGBP = msEURGBP.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURAUD = msEURAUD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURCHF = msEURCHF.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

int idxEURUSDn = DailyPeriodAdjustment(MarketSeries, idxEURUSD);

var idxUSDJPYn = DailyPeriodAdjustment(msUSDJPY, idxUSDJPY);

var idxGBPUSDn = DailyPeriodAdjustment(msGBPUSD, idxGBPUSD);

var idxAUDUSDn = DailyPeriodAdjustment(msAUDUSD, idxAUDUSD);

var idxUSDCHFn = DailyPeriodAdjustment(msUSDCHF, idxUSDCHF);

var idxEURJPYn = DailyPeriodAdjustment(msEURJPY, idxEURJPY);

var idxEURGBPn = DailyPeriodAdjustment(msEURGBP, idxEURGBP);

var idxEURAUDn = DailyPeriodAdjustment(msEURAUD, idxEURAUD);

var idxEURCHFn = DailyPeriodAdjustment(msEURCHF, idxEURCHF);

double yldEURUSD = ((MarketSeries.Close[idxEURUSD] - MarketSeries.Close[idxEURUSD - idxEURUSDn]) / MarketSeries.Close[idxEURUSD - idxEURUSDn]) * 10000;

double yldUSDJPY = ((msUSDJPY.Close[idxUSDJPY] - msUSDJPY.Close[idxUSDJPY - idxUSDJPYn]) / msUSDJPY.Close[idxUSDJPY - idxUSDJPYn]) * 10000;

double yldGBPUSD = -((msGBPUSD.Close[idxGBPUSD] - msGBPUSD.Close[idxGBPUSD - idxGBPUSDn]) / msGBPUSD.Close[idxGBPUSD - idxGBPUSDn]) * 10000;

double yldAUDUSD = -((msAUDUSD.Close[idxAUDUSD] - msAUDUSD.Close[idxAUDUSD - idxAUDUSDn]) / msAUDUSD.Close[idxAUDUSD - idxAUDUSDn]) * 10000;

double yldUSDCHF = ((msUSDCHF.Close[idxUSDCHF] - msUSDCHF.Close[idxUSDCHF - idxUSDCHFn]) / msUSDCHF.Close[idxUSDCHF - idxUSDCHFn]) * 10000;

double yldEURJPY = ((msEURJPY.Close[idxEURJPY] - msEURJPY.Close[idxEURJPY - idxEURJPYn]) / msEURJPY.Close[idxEURJPY - idxEURJPYn]) * 10000;

double yldEURGBP = ((msEURGBP.Close[idxEURGBP] - msEURGBP.Close[idxEURGBP - idxEURGBPn]) / msEURGBP.Close[idxEURGBP - idxEURGBPn]) * 10000;

double yldEURAUD = ((msEURAUD.Close[idxEURAUD] - msEURAUD.Close[idxEURAUD - idxEURAUDn]) / msEURAUD.Close[idxEURAUD - idxEURAUDn]) * 10000;

double yldEURCHF = ((msEURCHF.Close[idxEURCHF] - msEURCHF.Close[idxEURCHF - idxEURCHFn]) / msEURCHF.Close[idxEURCHF - idxEURCHFn]) * 10000;

if (!HideYeilds)

{

YldUSDJPY[index] = yldUSDJPY;

YldGBPUSD[index] = yldGBPUSD;

YldAUDUSD[index] = yldAUDUSD;

YldUSDCHF[index] = yldUSDCHF;

YldEURJPY[index] = yldEURJPY;

YldEURGBP[index] = yldEURGBP;

YldEURAUD[index] = yldEURAUD;

YldEURCHF[index] = yldEURCHF;

}

double usdidx0 = (yldUSDJPY + yldGBPUSD + yldAUDUSD + yldUSDCHF) / 4;

double euridx0 = (yldEURJPY + yldEURGBP + yldEURAUD + yldEURCHF) / 4;

double usdidx1 = USDIDX[index - 1];

double euridx1 = EURIDX[index - 1];

double USDdelta = usdidx0 - usdidx1;

double EURdelta = euridx0 - euridx1;

USDIDX[index] = usdidx0;

USDIDXPoints[index] = usdidx0;

EURIDX[index] = euridx0;

EURIDXPoints[index] = euridx0;

ActYld[index] = yldEURUSD;

ActYldPoints[index] = yldEURUSD;

ProjYld[index] = euridx0 - usdidx0;

ProjYldPoints[index] = euridx0 - usdidx0;

Delta[index] = EURdelta - USDdelta;

//if(USDdelta>0 && EURdelta<0 && -EURdelta>=USDdelta)SellSignal[index]=0;

//if(delta1<0 && delta2>0)BuySignal[index]=0;

CenterLine[index] = 0;

string USDTxt = string.Format("USD{0}", Math.Round(USDIDX[index], 0));

string EURTxt = string.Format("EUR{0}", Math.Round(EURIDX[index], 0));

string ACTTxt = string.Format("Act{0}", Math.Round(ActYld[index], 0));

string PROJTxt = string.Format("Pro{0}", Math.Round(ProjYld[index], 0));

ChartObjects.DrawText("USDlabel", USDTxt, index, USDIDX[index], VerticalAlignment.Center, HorizontalAlignment.Right, Colors.Green);

ChartObjects.DrawText("EURlabel", EURTxt, index, EURIDX[index], VerticalAlignment.Center, HorizontalAlignment.Right, Colors.Blue);

ChartObjects.DrawText("ACTlabel", ACTTxt, index, ActYld[index], VerticalAlignment.Top, HorizontalAlignment.Right, Colors.Yellow);

ChartObjects.DrawText("PROJlabel", PROJTxt, index, ProjYld[index], VerticalAlignment.Bottom, HorizontalAlignment.Right, Colors.Red);

}

private int DailyPeriodAdjustment(MarketSeries ms, int index)

{

if (index < 1) return 0;

int periods = 1;

DateTime CurrentDate = ms.OpenTime[index].AddHours(2);

DateTime PreviousDate = ms.OpenTime[index - periods].AddHours(2);

int DateDifference = (int)(CurrentDate.Date - PreviousDate.Date).TotalDays;

while (CurrentDate.DayOfWeek == PreviousDate.DayOfWeek || PreviousDate.DayOfWeek == DayOfWeek.Sunday || CurrentDate.DayOfWeek == DayOfWeek.Saturday)

{

periods++;

if (index < periods)

return periods - 1;

PreviousDate = ms.OpenTime[index - periods].AddHours(2);

DateDifference = (int)(CurrentDate.Date - PreviousDate.Date).TotalDays;

}

return periods - 1;

}

}

}

lec0456

Joined on 14.11.2012

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: myIndexEURUSD.algo

- Rating: 5

- Installs: 4526

- Modified: 13/10/2021 09:54

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

Thank you, this is a really nice strength indicator for finding you trades :)