Description

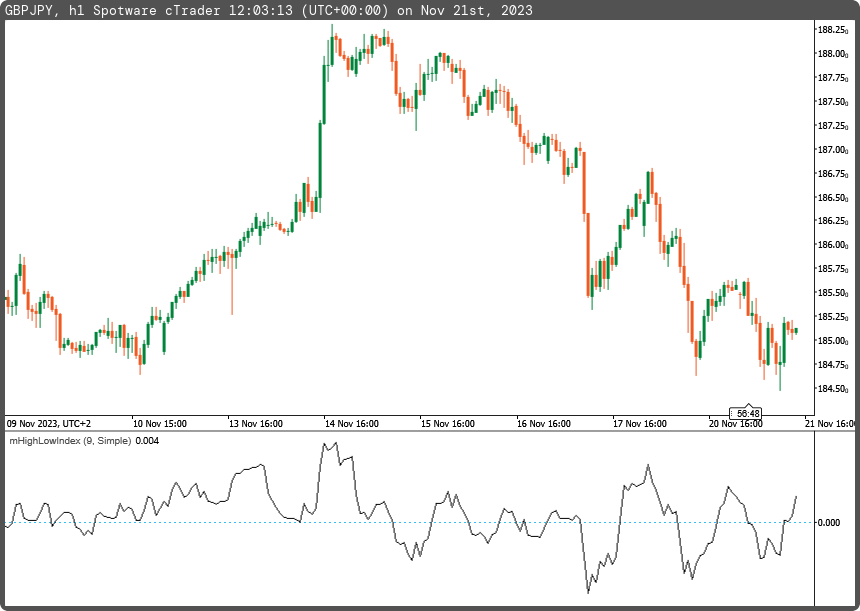

The High-Low Index is a breadth custom indicator based on the Record High Percent, which relies on new n-days highs and new n-days lows.

Use this indicator for a long zone when the indicator values are above the zero level. Also, use this indicator for a short zone when the indicator values are below the zero level.

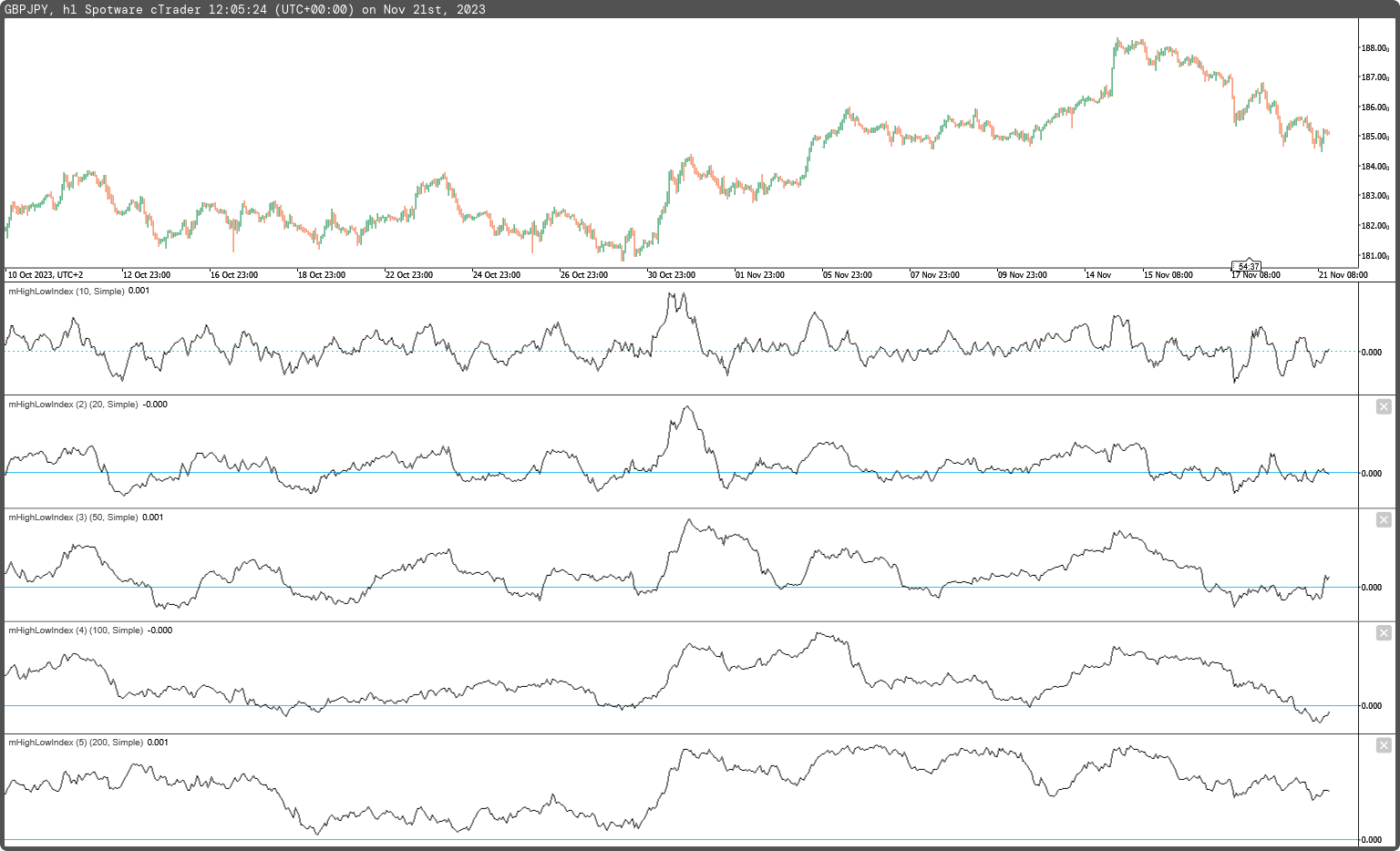

For more information about short-term and long-term price momentum pressure, this indicator is used in five periods (for example, 10, 20, 50, 100, 200; fig.2). Confluence in all different periods shows the exact direction of price movement in the near future. This method has been tested and used by my mentor, Iba.

using System;

using cAlgo.API;

using cAlgo.API.Internals;

using cAlgo.API.Indicators;

using cAlgo.Indicators;

namespace cAlgo

{

[Levels(0)]

[Indicator(IsOverlay = false, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class mHighLowIndex : Indicator

{

[Parameter("Periods (9)", DefaultValue = 9, MinValue = 2)]

public int inpPeriods { get; set; }

[Parameter("Smooth Type (sma)", DefaultValue = MovingAverageType.Simple)]

public MovingAverageType inpSmoothType { get; set; }

[Output("HighLowIndex avg", LineColor = "Black", LineStyle = LineStyle.Solid, Thickness = 1)]

public IndicatorDataSeries outHHLLavg { get; set; }

private IndicatorDataSeries _longdata, _shortdata;

private MovingAverage _longsmooth, _mashort;

protected override void Initialize()

{

_longdata = CreateDataSeries();

_shortdata = CreateDataSeries();

_longsmooth = Indicators.MovingAverage(_longdata, inpPeriods, inpSmoothType);

_mashort = Indicators.MovingAverage(_shortdata, inpPeriods, inpSmoothType);

}

public override void Calculate(int i)

{

_longdata[i] = (Bars.ClosePrices[i] / (Bars.ClosePrices[i] + Bars.LowPrices[i])) * 100;

_shortdata[i] = (Bars.ClosePrices[i] / (Bars.ClosePrices[i] + Bars.HighPrices[i])) * 100;

outHHLLavg[i] = (((_longsmooth.Result[i] + _mashort.Result[i]) / 2) - 50) / Symbol.PipSize;

}

}

}

mfejza

Joined on 25.01.2022

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: mHighLowIndex.algo

- Rating: 5

- Installs: 241

- Modified: 21/11/2023 12:23

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.