Description

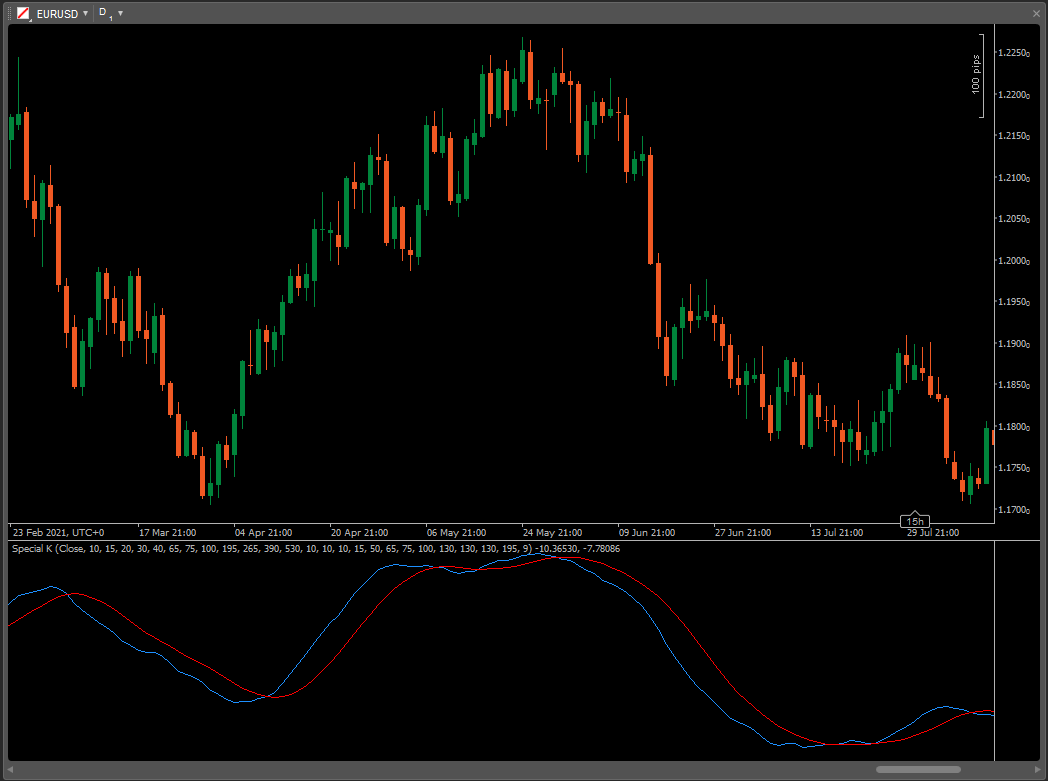

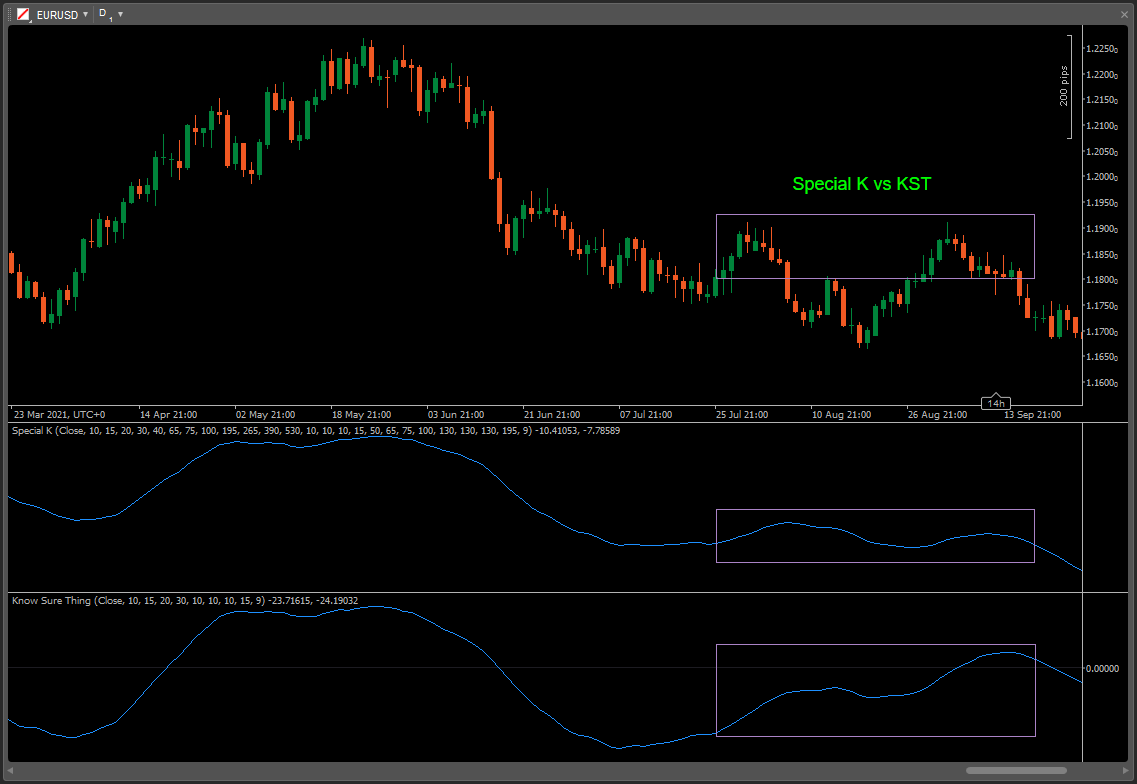

Created by Martin Pring, Special K is a momentum indicator that combines short-, intermediate- and long-term velocity into one complete series, thereby giving us true summed cyclicality. It has two functions: first, to identify primary trend reversals at a relatively early stage; second, to use that information for timing short-term pro-trend price moves.

Github: GitHub - Doustzadeh/cTrader-Indicator

using cAlgo.API;

using cAlgo.API.Indicators;

namespace cAlgo

{

[Levels(0)]

[Indicator(IsOverlay = false, AccessRights = AccessRights.None)]

public class SpecialK : Indicator

{

// Special K = 10 Period Simple Moving Average of ROC(10) * 1

// + 10 Period Simple Moving Average of ROC(15) * 2

// + 10 Period Simple Moving Average of ROC(20) * 3

// + 15 Period Simple Moving Average of ROC(30) * 4

// + 50 Period Simple Moving Average of ROC(40) * 1

// + 65 Period Simple Moving Average of ROC(65) * 2

// + 75 Period Simple Moving Average of ROC(75) * 3

// +100 Period Simple Moving Average of ROC(100)* 4

// +130 Period Simple Moving Average of ROC(195)* 1

// +130 Period Simple Moving Average of ROC(265)* 2

// +130 Period Simple Moving Average of ROC(390)* 3

// +195 Period Simple Moving Average of ROC(530)* 4

[Parameter("Source")]

public DataSeries Source { get; set; }

[Parameter("ROC1 Periods", Group = "ROC", DefaultValue = 10)]

public int RocPeriods1 { get; set; }

[Parameter("ROC2 Periods", Group = "ROC", DefaultValue = 15)]

public int RocPeriods2 { get; set; }

[Parameter("ROC3 Periods", Group = "ROC", DefaultValue = 20)]

public int RocPeriods3 { get; set; }

[Parameter("ROC4 Periods", Group = "ROC", DefaultValue = 30)]

public int RocPeriods4 { get; set; }

[Parameter("ROC5 Periods", Group = "ROC", DefaultValue = 40)]

public int RocPeriods5 { get; set; }

[Parameter("ROC6 Periods", Group = "ROC", DefaultValue = 65)]

public int RocPeriods6 { get; set; }

[Parameter("ROC7 Periods", Group = "ROC", DefaultValue = 75)]

public int RocPeriods7 { get; set; }

[Parameter("ROC8 Periods", Group = "ROC", DefaultValue = 100)]

public int RocPeriods8 { get; set; }

[Parameter("ROC9 Periods", Group = "ROC", DefaultValue = 195)]

public int RocPeriods9 { get; set; }

[Parameter("ROC10 Periods", Group = "ROC", DefaultValue = 265)]

public int RocPeriods10 { get; set; }

[Parameter("ROC11 Periods", Group = "ROC", DefaultValue = 390)]

public int RocPeriods11 { get; set; }

[Parameter("ROC12 Periods", Group = "ROC", DefaultValue = 530)]

public int RocPeriods12 { get; set; }

[Parameter("SMA1 Periods", Group = "SMA", DefaultValue = 10)]

public int SmaPeriods1 { get; set; }

[Parameter("SMA2 Periods", Group = "SMA", DefaultValue = 10)]

public int SmaPeriods2 { get; set; }

[Parameter("SMA3 Periods", Group = "SMA", DefaultValue = 10)]

public int SmaPeriods3 { get; set; }

[Parameter("SMA4 Periods", Group = "SMA", DefaultValue = 15)]

public int SmaPeriods4 { get; set; }

[Parameter("SMA5 Periods", Group = "SMA", DefaultValue = 50)]

public int SmaPeriods5 { get; set; }

[Parameter("SMA6 Periods", Group = "SMA", DefaultValue = 65)]

public int SmaPeriods6 { get; set; }

[Parameter("SMA7 Periods", Group = "SMA", DefaultValue = 75)]

public int SmaPeriods7 { get; set; }

[Parameter("SMA8 Periods", Group = "SMA", DefaultValue = 100)]

public int SmaPeriods8 { get; set; }

[Parameter("SMA9 Periods", Group = "SMA", DefaultValue = 130)]

public int SmaPeriods9 { get; set; }

[Parameter("SMA10 Periods", Group = "SMA", DefaultValue = 130)]

public int SmaPeriods10 { get; set; }

[Parameter("SMA11 Periods", Group = "SMA", DefaultValue = 130)]

public int SmaPeriods11 { get; set; }

[Parameter("SMA12 Periods", Group = "SMA", DefaultValue = 195)]

public int SmaPeriods12 { get; set; }

[Parameter("Signal Periods", DefaultValue = 9, MinValue = 1)]

public int SignalPeriods { get; set; }

[Output("Special K", LineColor = "DodgerBlue")]

public IndicatorDataSeries SK { get; set; }

[Output("Signal", LineColor = "Red")]

public IndicatorDataSeries Signal { get; set; }

private PriceROC Roc1, Roc2, Roc3, Roc4, Roc5, Roc6, Roc7, Roc8, Roc9, Roc10,

Roc11, Roc12;

private SimpleMovingAverage RCMA1, RCMA2, RCMA3, RCMA4, RCMA5, RCMA6, RCMA7, RCMA8, RCMA9, RCMA10,

RCMA11, RCMA12;

private SimpleMovingAverage SignalSMA;

protected override void Initialize()

{

Roc1 = Indicators.PriceROC(Source, RocPeriods1);

Roc2 = Indicators.PriceROC(Source, RocPeriods2);

Roc3 = Indicators.PriceROC(Source, RocPeriods3);

Roc4 = Indicators.PriceROC(Source, RocPeriods4);

Roc5 = Indicators.PriceROC(Source, RocPeriods5);

Roc6 = Indicators.PriceROC(Source, RocPeriods6);

Roc7 = Indicators.PriceROC(Source, RocPeriods7);

Roc8 = Indicators.PriceROC(Source, RocPeriods8);

Roc9 = Indicators.PriceROC(Source, RocPeriods9);

Roc10 = Indicators.PriceROC(Source, RocPeriods10);

Roc11 = Indicators.PriceROC(Source, RocPeriods11);

Roc12 = Indicators.PriceROC(Source, RocPeriods12);

RCMA1 = Indicators.SimpleMovingAverage(Roc1.Result, SmaPeriods1);

RCMA2 = Indicators.SimpleMovingAverage(Roc2.Result, SmaPeriods2);

RCMA3 = Indicators.SimpleMovingAverage(Roc3.Result, SmaPeriods3);

RCMA4 = Indicators.SimpleMovingAverage(Roc4.Result, SmaPeriods4);

RCMA5 = Indicators.SimpleMovingAverage(Roc5.Result, SmaPeriods5);

RCMA6 = Indicators.SimpleMovingAverage(Roc6.Result, SmaPeriods6);

RCMA7 = Indicators.SimpleMovingAverage(Roc7.Result, SmaPeriods7);

RCMA8 = Indicators.SimpleMovingAverage(Roc8.Result, SmaPeriods8);

RCMA9 = Indicators.SimpleMovingAverage(Roc9.Result, SmaPeriods9);

RCMA10 = Indicators.SimpleMovingAverage(Roc10.Result, SmaPeriods10);

RCMA11 = Indicators.SimpleMovingAverage(Roc11.Result, SmaPeriods11);

RCMA12 = Indicators.SimpleMovingAverage(Roc12.Result, SmaPeriods12);

SignalSMA = Indicators.SimpleMovingAverage(SK, SignalPeriods);

}

public override void Calculate(int index)

{

SK[index] = 1 * RCMA1.Result[index] + 2 * RCMA2.Result[index] + 3 * RCMA3.Result[index] + 4 * RCMA4.Result[index] + 1 * RCMA5.Result[index] + 2 * RCMA6.Result[index] + 3 * RCMA7.Result[index] + 4 * RCMA8.Result[index] + 1 * RCMA9.Result[index] + 2 * RCMA10.Result[index] + 3 * RCMA11.Result[index] + 4 * RCMA12.Result[index];

Signal[index] = SignalSMA.Result[index];

}

}

}

Doustzadeh

Joined on 20.03.2016

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: Special K.algo

- Rating: 0

- Installs: 1265

- Modified: 06/12/2021 06:46

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.