Description

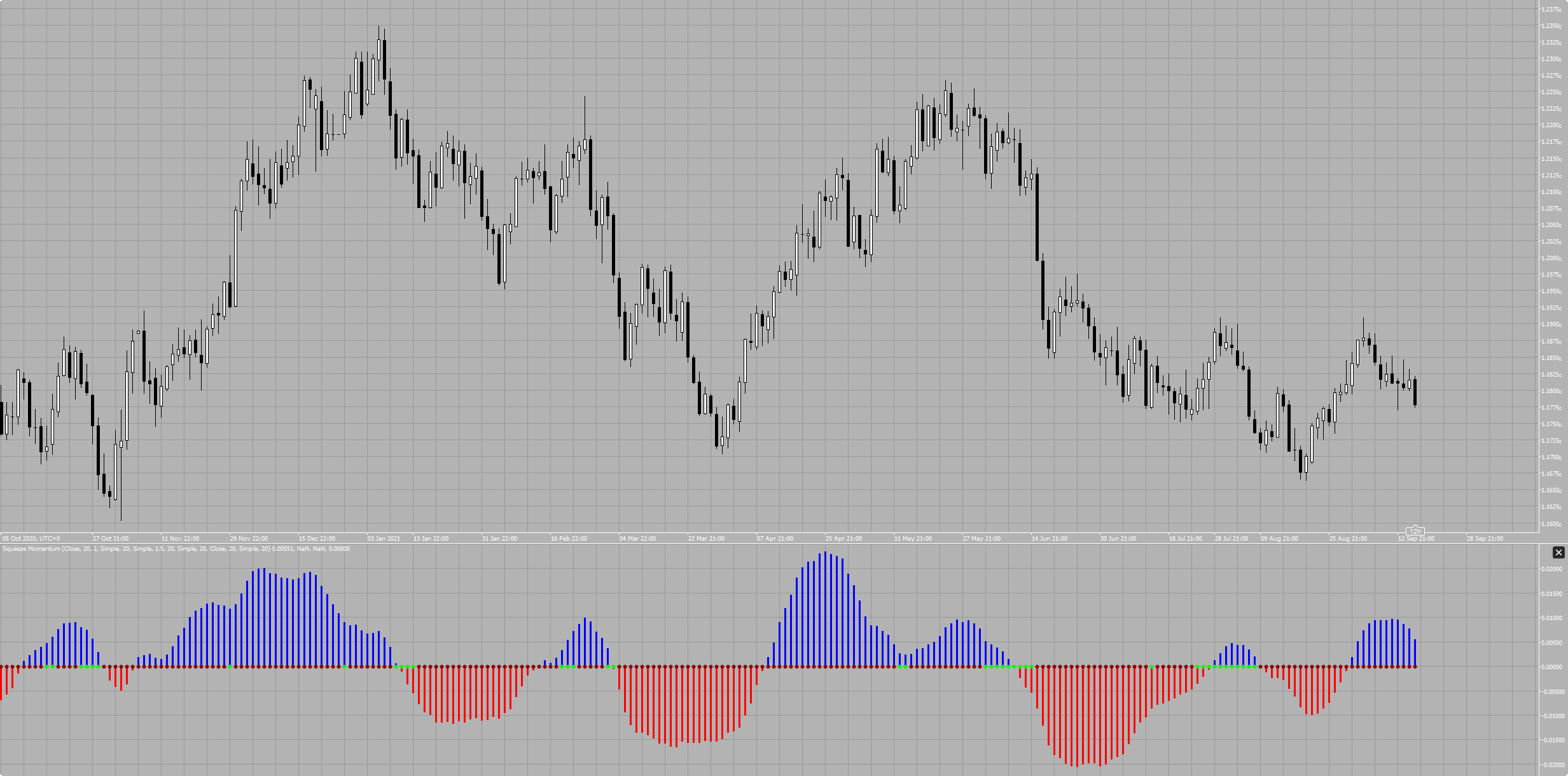

This is the John Carter Squeeze Momentum indicator implementation for cTrader.

Github:

using cAlgo.API;

using cAlgo.API.Indicators;

namespace cAlgo

{

[Indicator(IsOverlay = false, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class SqueezeMomentum : Indicator

{

private BollingerBands _bbands;

private KeltnerChannels _keltnerChannels;

private MovingAverage _ma;

private LinearRegressionForecast _linearRegression;

private IndicatorDataSeries _deltaSeries;

[Parameter("Source", Group = "Bollinger Bands")]

public DataSeries BollingerBandsSource { get; set; }

[Parameter("Periods", DefaultValue = 20, MinValue = 1, Group = "Bollinger Bands")]

public int BollingerBandsPeriods { get; set; }

[Parameter("Multiplier", DefaultValue = 2, MinValue = 0, Group = "Bollinger Bands")]

public double BollingerBandsMultiplier { get; set; }

[Parameter("MA Type", DefaultValue = MovingAverageType.Simple, Group = "Bollinger Bands")]

public MovingAverageType BollingerBandsMaType { get; set; }

[Parameter("MA Periods", DefaultValue = 20, MinValue = 1, Group = "Keltner Channels")]

public int KeltnerMaPeriods { get; set; }

[Parameter("MA Type", DefaultValue = MovingAverageType.Simple, Group = "Keltner Channels")]

public MovingAverageType KeltnerMaType { get; set; }

[Parameter("ATR Multiplier", DefaultValue = 1.5, MinValue = 0, Group = "Keltner Channels")]

public double KeltnerAtrMultiplier { get; set; }

[Parameter("ATR Periods", DefaultValue = 20, MinValue = 1, Group = "Keltner Channels")]

public int KeltnerAtrPeriods { get; set; }

[Parameter("ATR MA Type", DefaultValue = MovingAverageType.Simple, Group = "Keltner Channels")]

public MovingAverageType KeltnerAtrMaType { get; set; }

[Parameter("Midline Periods", DefaultValue = 20, MinValue = 1, Group = "Donchian")]

public int DonchianMidlinePeriods { get; set; }

[Parameter("Source", Group = "Moving Average")]

public DataSeries MaSource { get; set; }

[Parameter("Periods", DefaultValue = 20, MinValue = 1, Group = "Moving Average")]

public int MaPeriods { get; set; }

[Parameter("MA Type", DefaultValue = MovingAverageType.Simple, Group = "Moving Average")]

public MovingAverageType MaType { get; set; }

[Parameter("Periods", DefaultValue = 20, MinValue = 1, Group = "Linear Regression")]

public int LinearRegressionPeriods { get; set; }

[Output("Up Histogram Bars", LineColor = "Blue", PlotType = PlotType.Histogram, Thickness = 3)]

public IndicatorDataSeries UpHistogramBars { get; set; }

[Output("Down Histogram Bars", LineColor = "Red", PlotType = PlotType.Histogram, Thickness = 3)]

public IndicatorDataSeries DownHistogramBars { get; set; }

[Output("Squeeze On Dots", LineColor = "Lime", PlotType = PlotType.Points, Thickness = 5)]

public IndicatorDataSeries SqueezeOnDots { get; set; }

[Output("Squeeze Off Dots", LineColor = "DarkRed", PlotType = PlotType.Points, Thickness = 5)]

public IndicatorDataSeries SqueezeOffDots { get; set; }

protected override void Initialize()

{

_bbands = Indicators.BollingerBands(BollingerBandsSource, BollingerBandsPeriods, BollingerBandsMultiplier, BollingerBandsMaType);

_keltnerChannels = Indicators.KeltnerChannels(KeltnerMaPeriods, KeltnerMaType, KeltnerAtrPeriods, KeltnerAtrMaType, KeltnerAtrMultiplier);

_ma = Indicators.MovingAverage(MaSource, MaPeriods, MaType);

_deltaSeries = CreateDataSeries();

_linearRegression = Indicators.LinearRegressionForecast(_deltaSeries, LinearRegressionPeriods);

}

public override void Calculate(int index)

{

var donchianMidline = (Bars.HighPrices.Maximum(DonchianMidlinePeriods) + Bars.LowPrices.Minimum(DonchianMidlinePeriods)) / 2;

var donchainMidlineAndMaAverage = (donchianMidline + _ma.Result[index]) / 2;

_deltaSeries[index] = Bars.ClosePrices[index] - donchainMidlineAndMaAverage;

UpHistogramBars[index] = double.NaN;

DownHistogramBars[index] = double.NaN;

var linearRegression = _linearRegression.Result[index];

if (linearRegression > 0)

{

UpHistogramBars[index] = linearRegression;

}

else

{

DownHistogramBars[index] = linearRegression;

}

SqueezeOnDots[index] = double.NaN;

SqueezeOffDots[index] = double.NaN;

var isSqueezeOn = _bbands.Top[index] < _keltnerChannels.Top[index] && _bbands.Bottom[index] > _keltnerChannels.Bottom[index];

if (isSqueezeOn)

{

SqueezeOnDots[index] = 0;

}

else

{

SqueezeOffDots[index] = 0;

}

}

}

}

Spotware

Joined on 23.09.2013

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: Squeeze Momentum.algo

- Rating: 5

- Installs: 1954

- Modified: 13/10/2021 09:55

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.