Description

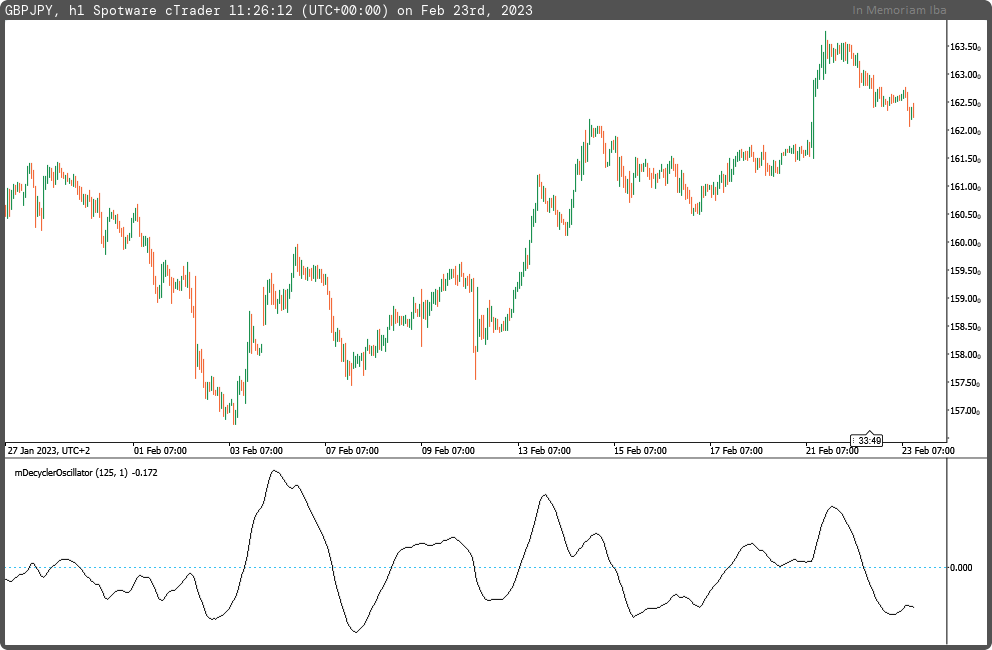

The Ehlers Decycler Oscillator is a technical indicator proposed by John F. Ehlers. Its calculation involves eliminating very low-frequency components from Ehlers Simple Decycler and transforming the output into the oscillator. Low-frequency components are eliminated using the half-period Ehlers Highpass filter.

The oscillator itself is equal to the ratio of the high-pass output data to price, multiplied by a coefficient. This coefficient is equal to 1 by default, however, you might want to adjust it if you use several instances of the oscillator on the same subgraph. Crossovers of oscillators with different coefficients might help identifying important trend reversals.

//John F.Ehlers Decycler Oscillator

using System;

using cAlgo.API;

using cAlgo.API.Collections;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo

{

[Levels(0)]

[Indicator(AccessRights = AccessRights.None)]

public class mDecyclerOscillator : Indicator

{

[Parameter("HP Period (125)", DefaultValue = 125)]

public int inpPeriodHP { get; set; }

[Parameter("Coefficient (1.0)", DefaultValue = 1.0)]

public double inpCoefficient { get; set; }

[Output("Decycler Oscillator", IsHistogram = false, LineColor = "Black", PlotType = PlotType.Line, LineStyle = LineStyle.Solid, Thickness = 1)]

public IndicatorDataSeries outDO { get; set; }

double angle1, angle2, alpha1, alpha2;

private IndicatorDataSeries _hp, _decycle, _decycle2;

private double a1, a2, a3, a4, b1, b2, b3, b4, pr2, pr3, pr4, pr5;

protected override void Initialize()

{

angle1 = 1.414 * 3.14159265358979323846 / inpPeriodHP;

angle2 = 2.0*angle1;

alpha1 = (Math.Cos(angle1) + Math.Sin(angle1) - 1.0) / Math.Cos(angle1);

alpha2 = (Math.Cos(angle2) + Math.Sin(angle2) - 1.0) / Math.Cos(angle2);

a1 = 1.0 - alpha1;

a2 = 1.0 - alpha1 / 2.0;

a3 = a1 * a1;

a4 = a2 * a2;

b1 = 1.0 - alpha2;

b2 = 1.0 - alpha2 / 2.0;

b3 = b1 * b1;

b4 = b2 * b2;

_hp = CreateDataSeries();

_decycle = CreateDataSeries();

_decycle2 = CreateDataSeries();

}

public override void Calculate(int i)

{

pr2 = 2.0 * (i>1 ? Bars.ClosePrices[i-1] : Bars.ClosePrices[i]);

pr3 = Bars.ClosePrices[i] - pr2 + (i>2 ? Bars.ClosePrices[i-2] : Bars.ClosePrices[i]);

_hp[i] = a4 * pr3 + (2.0 * a1 * (i>1 ? _hp[i-1] : 0)) - (a3 * (i>2 ? _hp[i-2] : 0));

_decycle[i] = Bars.ClosePrices[i] - _hp[i];

pr4 = 2.0 * (i>1 ? _decycle[i-1] : 0);

pr5 = _decycle[i] - pr4 + (i>2 ? _decycle[i-2] : 0);

_decycle2[i] = b4 * pr5 + (2.0 * b1 * (i>1 ? _decycle2[i-1] : 0)) - (b3 * (i>2 ? _decycle2[i-2] : 0));

outDO[i] = (Bars.ClosePrices[i]!=0 ? 100.0 * inpCoefficient * _decycle2[i] / Bars.ClosePrices[i] : 0);

}

}

}

mfejza

Joined on 25.01.2022

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: mDecyclerOscillator.algo

- Rating: 5

- Installs: 591

- Modified: 23/02/2023 11:33

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.